“What’s the UK job market like?”

The June 2026 KPMG & REC UK REPORT ON JOBS has been published featuring survey results from mid/late May.

The full report is posted here

A PDF of below is available here.

Jon Holt, Chief Executive and Senior Partner of KPMG in the UK commented:

“Ongoing global and domestic uncertainty is making businesses more cautious, and that is increasingly reflected in hiring decisions. While some employers are turning to temporary contracts to retain flexibility, many permanent hiring plans are being delayed or put on hold.

“Businesses need stability to plan and confidence to invest. With both still under pressure, the medium-term outlook for jobs remains subdued.”

Neil Carberry, REC Chief Executive, said:

“With businesses tapping the brakes on permanent hiring in the face of higher costs, the Gulf crisis and new employment red tape, temporary work is making up the gap…. backing our well-regulated temporary and contract workforce should be a priority for Government.”

Key UK job market findings are:

- Market uncertainty drives quicker reduction in permanent staff hiring

- Overall demand for staff falls at slightly quicker pace

- Permanent vacancies rose in London for a second month running

- Supply of labour continues to rise rapidly

- Pay growth remains tepid for both perm and temp staff

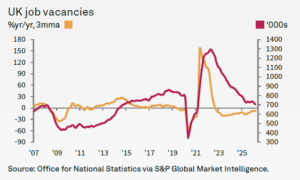

- ONS figures indicate that the number of total job vacancies across the UK fell again in the three months to April.

- Nursing/Medical/Care sector was the only monitored area to register higher demand for permanent staff

- The Retail and Hotel & Catering sectors again saw the steepest reductions in permanent vacancies.

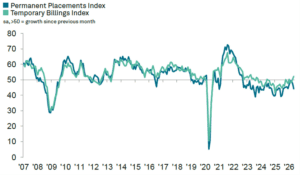

- Permanent placements fell across the UK as a whole during May, extending the current sequence of reduction to 44 months.

- Billings received from the employment of temp workers rose solidly across the UK in May, with the rate of growth the most pronounced in 37 months.

Appointments

Permanent placements decline sharply in May, temp billings expand at quickest pace in over three years.

After adjusting for seasonal factors, the Permanent Placements Index declined further in May, remaining below the 50.0 no-change threshold and indicating a more pronounced fall in permanent hiring activity across the UK. The rate of contraction was the fastest recorded since July of last year. Respondents attributed the weakness in recruitment to heightened economic uncertainty and subdued business confidence, which prompted many employers to delay hiring decisions. Others reported that rising employment costs had placed additional pressure on recruitment budgets.

Permanent placements have now decreased continuously for 44 consecutive months, representing by far the longest sustained downturn since the survey’s inception in 1997.

Regional data showed significant reductions in permanent recruitment throughout the Midlands and Southern England, while London experienced a renewed and notable decline. In contrast, the North of England was the only area to register growth, albeit at a modest level.

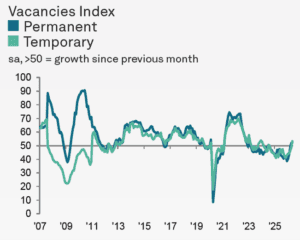

Vacancies

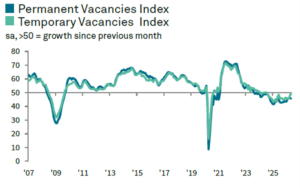

Vacancies fall at fastest rate in three months

After moderating over the previous four months, the decline in hiring demand gathered pace again in May. The seasonally adjusted Total Vacancies Index fell from 46.2 to 45.9, signalling a solid reduction in overall job openings and the sharpest contraction in vacancies since February.

However permanent hiring demand in London increased for the second consecutive month in May. The rate of expansion was solid and represented the strongest growth in permanent vacancies since 2022.

Permanent and temporary vacancies

The weakening in overall recruitment demand was largely attributable to a more significant fall in permanent vacancies. Demand for permanent hires declined at its fastest rate in four months during May. By contrast, temporary vacancies continued to edge lower, although the rate of decline was modest and the least severe recorded during the current 22-month downturn.

Public and private sector vacancies

A similar pattern was evident across both public and private sector employers in May. Permanent vacancies saw notable declines, while demand for temporary workers slipped only marginally.

The most significant reduction in hiring activity was reported for permanent positions within the private sector.

Vacancies by Sector

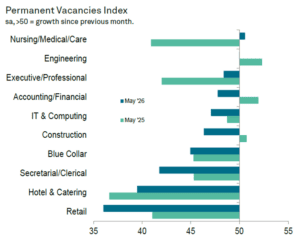

The Nursing, Medical and Care sector was the sole area monitored to record an increase in demand for permanent employees during May. Demand remained unchanged within Engineering, while all other sectors reported lower vacancy levels. The most significant decline in permanent hiring activity was observed in the Retail sector.

Demand for temporary workers increased across four of the ten sectors monitored in May, with the Blue Collar category experiencing the most notable rise in vacancies. In contrast, the Retail sector reported the steepest decline in demand for temporary staff, falling at a considerably faster rate than any other category.

ONS Data

Office for National Statistics showed that total job vacancies across the UK continued to decline in the three months to April. The number of available positions stood at 705,000, representing a 7.1% decrease compared with the same period a year earlier. This was the lowest vacancy figure recorded for five years and, excluding the pandemic period, the weakest level seen in more than eleven years.

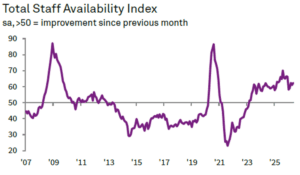

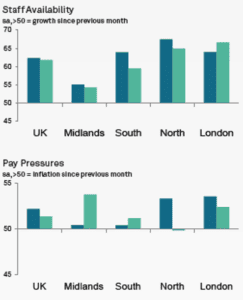

Staff availability

Overall candidate supply increases at faster pace

The availability of candidates seeking employment continued to increase during May. The seasonally adjusted index rose from 61.0 in April to 62.3, indicating a stronger and sustained expansion in candidate supply, although growth remained below the average levels seen throughout 2025.

Data also showed that both permanent and temporary labour pools expanded at a faster pace during the month, reflecting a broader increase in the number of individuals actively looking for work.

The supply of permanent candidates increased at a faster rate in May, marking the third acceleration in growth over the past four months. The seasonally adjusted Permanent Staff Availability Index continued to indicate a strong rise in the number of jobseekers, although the pace remained below the average levels recorded during 2025.

Survey participants reported that ongoing redundancies remained a significant factor behind the increase in candidate availability. In addition, more individuals were said to be exploring alternative employment opportunities due to concerns about the stability of their current roles.

Regionally, the North of England recorded the strongest growth in candidate availability, while the Midlands experienced the most modest increase.

Pay pressures

Permanent starters’ pay continues to rise modestly

Data collected in May pointed to another increase in average starting salaries for permanent employees across the UK, extending the current run of salary growth to 63 consecutive months. The rate of increase remained modest and was broadly unchanged from April, continuing to track below the survey’s historical average.

Employers reporting higher starting salaries often cited strong competition for specialist skills, alongside the ongoing impact of rising living costs. Nevertheless, softer hiring activity, an expanding pool of available candidates and tighter budgetary controls helped to restrain overall pay growth.

At a regional level, London recorded the most significant increase in starting salaries during the month.

ONS Data

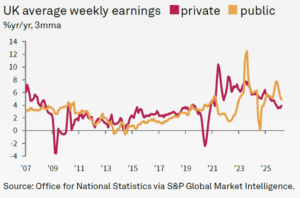

Latest data from the Office for National Statistics (ONS), showed that total employee earnings, including bonuses, increased by 4.1% compared with a year earlier in the three months to March 2026. Although this represented a modest improvement on the 3.9% growth recorded in the previous three-month period, it remained one of the weakest rates of earnings growth seen since the pandemic.

A slight acceleration in private sector pay growth, which rose to 3.9% from 3.6%, helped support the overall increase. This was partly offset by a moderation in public sector earnings growth, which eased to 4.9% from 5.2% in the preceding period.

London job market

KPMG and REC also produce a London job market analysis.

Anna Purchas, London Office Senior Partner at KPMG UK, said:

“While permanent placements dipped during the month, demand for staff strengthened significantly, with permanent vacancies rising at their fastest rate in more than three and a half years and temporary vacancies returning to growth for the first time since 2024. That combination points to a labour market that is gathering momentum”

A renewed fall in permanent placements in May

Recruitment firms in London reported a renewed decline in permanent hiring activity during May. While the decrease was moderate in scale and less pronounced than the national average, it marked the first fall in permanent placements since February.

According to respondents, lower levels of client demand and ongoing uncertainty in the market were the principal factors behind the reduction in permanent recruitment.

Job vacancies

However permanent hiring demand in London increased for the second consecutive month in May. The rate of expansion was solid and represented the strongest growth in permanent vacancies since October 2022. Notably, London was the only one of the four English regions monitored to record an increase in permanent job opportunities.

It was not clear from the report why vacancies rose but placement didn’t.

Demand for temporary workers also strengthened, rising for the first time in 22 months. Temporary vacancies increased at a solid pace, with growth reaching its highest level in almost two and a half years.

Marked rise in permanent staff supply

London continued to experience an increase in the availability of permanent candidates during May, extending the trend that has been in place since December 2022. The pace of growth accelerated compared with April and was substantial overall. Recruiters frequently attributed the rise in candidate numbers to ongoing redundancies across the market.

Among the four English regions monitored, only the North of England recorded a faster increase in permanent labour supply than London during the month.

Sustained growth in starting salaries

Average starting salaries for newly appointed permanent employees in London increased at a moderate pace during May. The rate of salary growth was largely unchanged from April and remained relatively subdued by historical standards, although it was the strongest recorded among the four English regions monitored.

Recruiters reported that employers were offering higher salaries in order to secure and attract suitably qualified talent in a competitive market.

Regional comparison

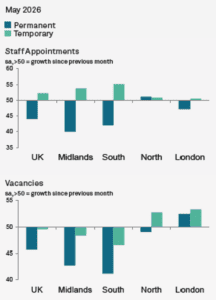

Staff appointments

Permanent hiring activity continued to weaken across the UK in May, marking the 44th consecutive month of decline. The rate of contraction accelerated to its fastest level since July last year and remained significant overall. The downturn was driven primarily by substantial reductions in the Midlands and the South of England, with London also reporting lower placement volumes. In contrast, the North of England was the only region to record growth, although the increase was modest and the weakest seen in four months.

Revenue generated from temporary placements increased strongly across the UK during May, with the pace of growth reaching its highest level in 37 months. Notably, all regions reported an increase in temporary billings for the first time since December 2022. The South of England led the way with the strongest growth, followed by the Midlands, while both London and the North of England recorded renewed, albeit relatively modest, expansions.

Candidate availability

Recruiters across the UK reported a further rise in the availability of permanent candidates during May. The rate of increase accelerated compared with April and remained strong overall, although it was still below the levels typically recorded throughout 2025. All monitored English regions, with the exception of the Midlands, experienced marked and faster growth in candidate numbers. The Midlands recorded the most modest increase.

The supply of temporary workers also expanded at a stronger pace during May. Growth accelerated to its fastest level in six months, reflecting a broad increase in candidate availability across the UK. London recorded the most significant rise in temporary labour supply, while the Midlands once again saw the weakest rate of growth.

Pay pressures

Starting salaries for newly appointed permanent employees continued to rise across the UK in May, extending the period of salary inflation that has been in place since March 2021. However, the pace of growth was broadly unchanged from April and remained relatively subdued by historical standards. London recorded the strongest increase in starting salaries, closely followed by the North of England. The Midlands and the South of England registered the weakest rates of salary growth.

Average hourly pay rates for temporary workers also increased during May, although the rate of growth was modest and below the survey’s long-term average. Three of the four English regions monitored reported higher temporary pay, with the Midlands recording the strongest uplift. In contrast, temporary wages in the North of England edged down slightly over the month.

The Prism Executive Recruitment perspective: management consultancy recruitment

The Decline in the Management Consulting Job Market

The management consulting recruitment market has been under considerable pressure since late 2022. From the middle of 2023 onwards, the Big Four firms and many other major consultancies, including strategy houses that have historically been more insulated from downturns, announced multiple rounds of job reductions. At the same time, a significant number of smaller consulting firms have quietly trimmed both their permanent headcount and associate networks.

The result has been a substantial imbalance between the number of experienced consultants seeking work and the volume of available opportunities. Many consulting employers simply do not have enough open positions to absorb the growing pool of unemployed management consultants.

Throughout 2024 and 2025, a series of high-profile announcements reinforced the challenging market conditions. In May 2024, media reports highlighted that “PwC asks for silence from departing staff in programme of UK job cuts,” reflecting another sizeable voluntary redundancy exercise.

The following month brought further concerns, with reports that “Consultants to lose £3bn of UK government work under plan to halve advisory spend.”

By July 2024, the Financial Times observed that “UK consultant numbers shrink as companies cut back on external advice. Headcount fell 3% last year with firms axing jobs and moving staff as post-pandemic boom fades.”

Redundancy announcements continued later in the year. In October, reports stated that “Deloitte axes 250 UK employees in performance-related cull.” This was followed in December by news that “Deloitte accelerates UK layoffs with fresh redundancy round.”

EY also announced proposed workforce reductions in December 2024, stating that “Regrettably, proposals put forward in part of the UK consulting practice may result in a reduction of 150 roles”.

The negative news flow persisted into 2025. Among the more notable headlines were “PwC UK cuts jobs as revenue growth slows sharply” and “Deloitte UK’s revenues fall for first time in 15 years” in September. Earlier in the year, in June, concerns about client demand were highlighted when “Accenture says CEOs are postponing hiring consultants due to uncertainty”.

There are however some slightly more encouraging signs in 2026 with headlines including:

“Consultancies set for fastest growth in years on back of AI boom”

“Consultants cash in on Europe’s defence pivot”

And, in a sign that AI isn’t leading to a “jobs apocalypse”…

“Human skills ‘matter even more’ for early consultancy career roles”

Potential Reasons for the Downturn:

- Overly Optimistic Hiring and pay rises in 2022: Many firms hired extensively, dangling salary increases which have added to costs, expecting sustained growth that ultimately did not materialise.

- Economic Slowdown since: The consultancy sector is highly responsive to economic shifts and even a mild downturn can prompt hiring freezes and lead to subsequent redundancies.

- Cautious Expansion: Although many firms continue to perform reasonably well, ongoing uncertainty has made them hesitant to increase their headcount.

- Sector Growth Slowing: in January 2026 a survey of UK consulting leaders projected growth of 5.7% in 2026, the lowest rate since 2020.

Other indicators

In related news:

- The NatWest UK Regional Growth Tracker from mid May says “Seven out of 12 UK nations and regions record growth, led by London and North East. Rates of business cost inflation reach multi-year highs, drive up prices charged for goods and services. Employment falls in most areas as firms report declining backlogged orders”

- The Lloyds Bank Business Barometer from May 2026 states “UK business confidence edged higher in May, indicating tentative stabilisation after April’s sharp decline. The headline index rose 3 points to 47%, with modest improvements in both trading prospects and economic expectations. Cost pressures and economic uncertainty remained key headwinds, though some firms continued to report resilient demand and a willingness to invest. Staffing expectations eased for a second consecutive month, signalling a moderation in hiring rather than outright job cuts. Firms appear to be balancing recruitment needs against persistent cost pressures and increased automation.”

- The IoD Directors’ Economic Confidence Index, from 1 June which measures business leader optimism over prospects for the UK economy, said “Business confidence improves despite rising concerns about Iran conflict” and rose to -53 in May 2026 from -64 in April. Business leader confidence in their own organisations also rose, to +23 in May from +8 in April. This is the highest reading since August 2024 (+23). Most of the underlying indicators also improved albeit there was reference to “widespread frustration with tax and regulatory burdens, particularly employment.”

- While the CIPD’s Spring 2026 Labour Market Outlook released in May states “this quarter’s data indicates a broadly stable jobs market, with marginally more positive recruitment activity in the public sector. Our data, collected across March and April, does not show any material impact of the recent conflict in Iran on our employment indicators; however, as with any geopolitical shock, it can take businesses a period of time to assess the potential impact on their operations.”

- The Page Group, very much an economic bellwether in professional and executive hiring, issued a Q1 trading update in April 2026 stating “Ongoing subdued levels of client and candidate confidence impacting decision making…continued tough market conditions in EMEA and the UK ….strong performances from Americas and Asia Pacific”

- BDO’s Employment Index published in early March 2026 suggests that hiring intentions are at the lowest level for 15 years.

- On 30 April 2026 the comprehensive Adzuna UK Job Market Report stated “UK job vacancies showed signs of recovery in March, rising +3.74% month-on-month to 752,711 – marking the second consecutive monthly increase after an extended period of decline” along with other broadly positive indicators.

- The REC’s Labour Market Tracker, which reviews job postings, updated in May 2026, shows a level broadly unchanged since September 2024.

- The most recent quarterly ManpowerGroup Employment Outlook Survey , released in June on the state of the labour market globally for Q3 2026 puts the UK well above average with regard to hiring expectations.

- A June LinkedIn report states UK hiring fell by 24% between January 2019 and January 2026. The professional networking site said the decline was largely down to employers being more cautious about recruitment amid geopolitical and trade uncertainty, rather than a consequence of the shift towards AI. “There is high demand for talent that can combine AI literacy with crucial human skills, such as collaboration and creativity – this is what will help to give companies the edge as the economy recovers”

Methodology

The KPMG and REC UK Report on Jobs is compiled by S&P Global from responses to questionnaires sent to a panel of around 400 UK recruitment and employment consultancies.

For more information on the job market, or to discuss your hiring or career plans please contact Chris Sale, Managing Director, Prism Executive Recruitment via [email protected]