“What’s the UK job market like?”

The May 2025 KPMG & REC UK REPORT ON JOBS has been published featuring survey results from mid/late April.

The full report is posted here while a PDF version of this article is here.

Jon Holt, Chief Executive and Senior Partner of KPMG in the UK commented:

“A softening in the pace of the hiring slowdown failed to bring any significant green shoots for the jobs market in April, as recruitment continued to be muted and the number of people looking for jobs increased. …businesses will be looking for more signs of market stability before committing to any major spending.”

Neil Carberry, REC Chief Executive, said:

“Given the bow wave of costs firms faced in April, maintaining the gradual improvement in numbers we have seen over the past few months is on the good end of our expectations. While we are yet to see real momentum build, hopes of an improving picture in the second half of the year should be buoyed by today’s data. ”

Key findings are:

- April sees softer fall in recruitment activity

- Candidate supply continues to rise rapidly

- Temp wage growth improves

- Demand for staff continues to decline sharply

- ONS vacancy figures the lowest recorded since the three months to May 2021

- Nursing/Medical/Care, Hotel & Catering and Retail sectors saw the steepest reductions in permanent vacancies.

- All four monitored English regions noted a fall in permanent staff appointments, with the strongest downturn seen in the South of England.

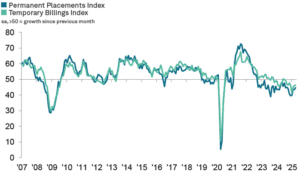

Appointments

Permanent placements fall at softest pace in seven months

Recruitment firms across the UK reported another drop in the number of candidates placed in permanent positions during April, extending the ongoing downturn to 31 consecutive months. Many contributors noted that employers were showing increased caution towards committing to long-term hires, citing heightened economic uncertainty as a key factor.

Additional feedback pointed to budgetary constraints and rising payroll costs as further deterrents to recruitment activity. Although the decline remained significant, it was the least severe recorded since last September.

Regionally, the South of England saw the most pronounced fall in permanent placements, while London experienced the gentlest decrease.

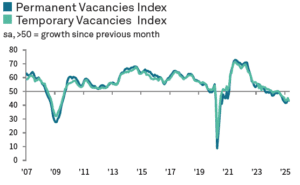

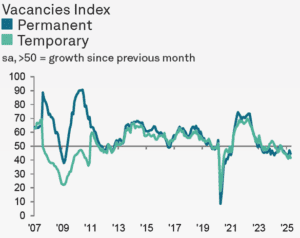

Vacancies

Further steep reduction in demand for workers

Job vacancies in the UK fell for the sixteenth consecutive month in February. The decline remained steep, marking the second-fastest rate of contraction since August 2020, with the seasonally adjusted index rising only marginally.

Permanent & temporary vacancies

The seasonally adjusted Total Vacancies Index declined to 43.1 in April from 44.2 in March, pointing to a continued fall in overall demand for staff for the eighteenth month running. While the rate of decline was less severe than in January and February 2025, the index still reflected a historically sharp downturn.

April’s data indicated a faster rate of contraction in both permanent and temporary staff demand, with both seeing comparably steep decreases. Notably, temporary job openings shrank at the quickest pace recorded since June 2020.

Public & private sector vacancies

Sector-specific data showed that the public sector experienced more pronounced reductions in job vacancies compared to the private sector. The sharpest drop was reported for permanent public sector roles, while the smallest—though still considerable—decline was registered in temporary private sector positions.

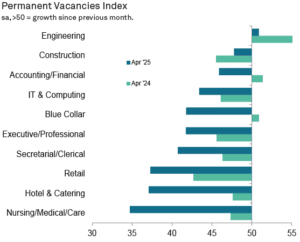

Vacancies by Sector

Engineering was the sole job category among those tracked to record a rise in demand for permanent staff during April, though the increase was only slight.

In contrast, the sharpest declines in permanent vacancies were reported across the Nursing/Medical/Care, Hotel & Catering, and Retail sectors. The former is unprecedented as the sector has historically been resilient.

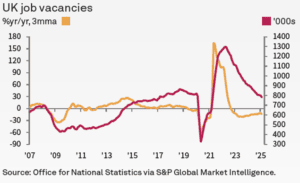

ONS Data

Office for National Statistics There were an estimated 781,000 job vacancies across the UK in the three months leading up to March, marking a decrease of 26,000 compared to the previous three-month period and the lowest level seen since the three months ending May 2021.

Importantly, this total was around 5% below the pre-pandemic figure, which stood at 819,000 vacancies in the three months to February 2020.

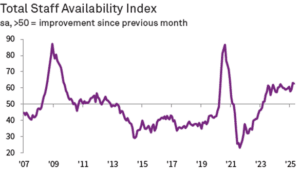

Staff availability

Continued sharp rise in overall candidate availability

The seasonally adjusted Total Staff Availability Index registered 62.6 in April, down marginally from 63.0 in March, indicating a strong increase in the supply of candidates— the second-quickest rate since December 2020. This latest rise extended the ongoing trend of growing staff availability to 26 consecutive months.

Recruitment consultancies across the UK reported another rise in the availability of candidates for permanent roles in April. The pace of growth remained near the 51-month high seen in March. According to respondents, the increase in supply was frequently linked to redundancies and organisational restructuring. A decline in vacancy numbers was also cited, alongside reports of individuals proactively searching for new roles amid job security concerns or in pursuit of better pay.

All four English regions covered by the survey saw substantial growth in the number of permanent jobseekers.

Pay pressures

Permanent starting salaries grow, but remain below long-term average

April marked the fiftieth consecutive month of rising salaries for newly hired permanent staff. While the rate of increase matched March’s seven-month peak and remained firm, it continued to fall short of the long-term average.

Recruiters cited the need to attract and retain skilled candidates as a key driver of salary growth, with some employers also boosting pay in response to recent hikes in the national minimum and living wage.

All four surveyed English regions reported starting salary increases, with the strongest growth seen in the Midlands.

ONS Data

According to the latest data from the Office for National Statistics (ONS), average weekly earnings grew at a historically robust rate in the three months to February, holding steady at 5.6%—the same pace as the previous three-month period. This figure was nearly twice the pre-pandemic average of 2.9%.

Pay growth in the public sector edged slightly ahead of the private sector, at 5.7% compared to 5.6%. Significantly, this marked the fastest increase in public sector pay since the three months to May 2024.

London job market

KPMG and REC also produce a London job market analysis.

Fresh downturn in permanent placements reverses growth seen in March

After seeing an increase in March—the first in eight months—London-based recruitment firms reported a decline in permanent placements during April. Panellists attributed the downturn to market uncertainty and a reduction in available roles.

That said, the drop in hiring was relatively mild and represented the slowest rate of decline among the four English regions surveyed.

Job vacancies

Job vacancies in London saw a marked decline in April, with contractions in both permanent and temporary roles accelerating from the previous month.

Although the capital experienced the mildest fall in permanent vacancies among the four English regions, the drop in temporary roles was the second-steepest, exceeded only by the South of England.

Significant but less steep rise in permanent candidate availability

Permanent candidate availability in London continued to rise in April, maintaining a trend that began in December 2022. Although the pace of growth eased significantly from March’s recent peak, it remained substantial overall.

The increase was largely attributed to redundancies and a slowdown in hiring activity. Among the four English regions monitored, only the South of England saw a slower rate of growth in permanent staff supply than London.

Permanent starting salary growth eases to three-month low

Continuing the trend seen since March 2021, starting salaries for new permanent hires in London increased again in April. However, the pace of growth slowed to its weakest level in three months.

Of the four English regions monitored, the Midlands saw the sharpest rise in starting pay, with London recording the second fastest increase.

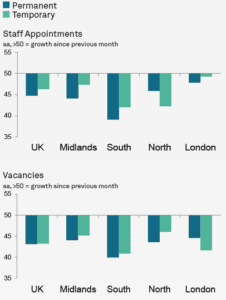

Regional comparison

Staff appointments

Permanent staff hires continued to decline across the UK at the beginning of the second quarter, extending a downward trend that has persisted since October 2022. Although the rate of decline slowed to its weakest in seven months, it remained significant. All four English regions saw reductions in permanent placements, with the sharpest fall recorded in the South of England.

Temporary billings also dropped for the tenth month in a row during April, showing a solid overall decline. All monitored regions reported decreases, again led by the South. In contrast, London saw only a slight fall in temp billings.

Candidate availability

Permanent staff availability grew strongly across the UK at the start of Q2, with the pace of expansion the second-fastest since December 2020. The North of England led the increase, though notable rises were also reported in the other three English regions.

Temporary candidate supply also rose sharply in April. Although the rate of growth slowed from March, it remained brisk overall. The South of England saw the fastest increase in temp availability, while the Midlands recorded the most modest rise.

Pay pressures

Starting salaries for permanent roles increased moderately at the national level in April, with the pace of growth matching that seen in March. The Midlands posted the strongest rise in starting pay, and the South of England the weakest. Notably, all four English regions saw permanent salary increases for the first time in six months.

Meanwhile, hourly pay for temporary workers rose solidly across the UK, reaching the fastest rate of growth in nearly a year. All monitored regions reported quicker increases in temp pay, led by the South of England.

The Prism Executive Recruitment perspective: management consultancy recruitment

The Decline in the Management Consulting Job Market

The job market in management consulting has declined significantly in the last two years. Indeed since mid-2023, the Big Four and other leading consultancies, including typically resilient strategy firms, have publicly announced redundancies. Numerous smaller firms have been quietly reducing their permanent teams or associates.

At present, few consulting employers have sufficient vacancies to absorb the large number of unemployed management consulting professionals.

In May 2024, headlines highlighted “PwC asks for silence from departing staff in programme of UK job cuts,” signalling another significant round of voluntary redundancies.

In June, it was reported that “Consultants to lose £3bn of UK government work under plan to halve advisory spend.”

By July 2024, the Financial Times noted, “UK consultant numbers shrink as companies cut back on external advice. Headcount fell 3% last year with firms axing jobs and moving staff as post-pandemic boom fades.”

In October, “Deloitte axes 250 UK employees in performance-related cull.” and in December “Deloitte accelerates UK layoffs with fresh redundancy round”.

EY meanwhile in December stated “Regrettably, proposals put forward in part of the UK consulting practice may result in a reduction of 150 roles”

Reasons for the Downturn:

- Overly Optimistic Hiring and pay rises in 2022: Many firms hired extensively, dangling salary increases which have added to costs, expecting sustained growth that ultimately did not materialise.

- Economic Slowdown in 2023 and 2024: The consultancy sector is highly responsive to economic shifts and even a mild downturn can prompt hiring freezes and lead to subsequent redundancies.

- Cautious Expansion: Although many firms continue to perform reasonably well, ongoing uncertainty has made them hesitant to increase their headcount.

- Sector Growth Slowing: in January 2025: a survey among the member-firms of the Management Consultancies Association reveals that many expect revenue expansion to be just 6.4% in the coming 12 months, the lowest rate since 2020.

- With no sign of a turnaround: here from early May “PwC to slash 1,500 US jobs” while in March “PwC cuts record number of UK partners and halts tech apprenticeship scheme”.

Other indicators

In related news:

- On the same day as the KPMG/REC report came the welcome news that the economy performed notably better than some of the more pessimistic forecasts for the first quarter of the year. While some predicted a recession, the growth rate of 0.7% exceeded expectations. This suggests a possible return to more stable and sustainable growth levels.

- The latest NatWest UK Regional Growth Tracker published 10 April 2025 states “Improved business growth in more regions of the UK at the end of Q1 – but the majority are still being affected by wider economic uncertainty.”

- The S&P Global UK Manufacturing Purchasing Managers’ Index (PMI) states “Manufacturing downturn continues as business confidence falls and cost inflation hits near two-and-a-half year peak…Output, new orders and employment all decrease” while the UK Services Purchasing Managers’ Index states “Business activity falls for the first time since October 2023”

- The Lloyds Bank Business Barometer states “After a strong first quarter, business confidence plummeted in April, driven by a significant drop in economic optimism and weaker trading prospects. The headline confidence index fell by 10 points to 39%, marking the lowest level in three months and the largest one-month decline since June 2022”

- The BDO Business Trends from May 2025 states “The latest Business Trends report reveals UK employment has reached a new 12-year low as businesses grapple with rising labour costs and global uncertainty. This drop in the BDO Employment Index signals further cooling of the UK jobs market, with vacancies continuing to decline in Q1 and falling below pre-pandemic levels for the first time in four years.”

- The IoD Directors’ Economic Confidence Index, from 1 May offers a glimmer of hope: “ The IoD Directors’ Economic Confidence Index, which measures business leader optimism in prospects for the UK economy, rose slightly for the second month in a row, from -58 in March 2025 to –51 in April – the highest since September 2024”. Clearly still significantly negative however.

- In April Reed’s job market review reported: “112,990 jobs were posted on Reed.co.uk in March, up +8% month-on-month, but significantly below the 160,378 jobs posted in March 2024”

- While the CIPD’s Spring Labour Market Outlook states “Employer confidence has fallen again this quarter, with the net employment balance dropping to +8 – the lowest level recorded outside the pandemic. Hiring intentions have weakened, and one in four employers now plan redundancies.”

The Page Group, very much an economic bellwether in professional and executive hiring, issued preliminary results in March 2025 with operating profit halved at £52.4m (2023: £118.8m) stating “Market conditions remained challenging across all regions in 2024, with worsening sentiment and reduced confidence in Europe during the second half of the year”

IWOCA, the business loans company, in March reported on their survey which suggested that over 300,000 SMEs may cut jobs due to rising employer National Insurance contributions (NICs)

The REC’s Labour Market Tracker, which reviews job postings, updated in April, shows a level comparable with Q4 2024.

The most recent quarterly ManpowerGroup Employment Outlook Survey , on the state of the labour market in UK Q2 2025 says:

“UK employers are continuing to kick major hiring decisions into the long grass, with the latest data from the ManpowerGroup Employment Outlook Survey showing 42% of organisations plan no changes to their employee headcount in Q2 (April – June) 2025. An additional 11% don’t know if or how their staffing levels will change. Among employers who are planning headcount changes, average employer hiring volume is down -27% versus Q1 2025”

Methodology

The KPMG and REC UK Report on Jobs is compiled by S&P Global from responses to questionnaires sent to a panel of around 400 UK recruitment and employment consultancies.

For more information on the job market, or to discuss your hiring or career plans please contact Chris Sale, Managing Director, Prism Executive Recruitment via [email protected]